Earnings Week 10/18 - 10/22

And so earnings season is back.

Hey reader! 📰

If you’re new here, welcome and if not, welcome back! If you haven’t joined the 412 subscribed members yet and would like to get an earnings summary each Saturday during each earnings season, you can sign up below for FREE.

A friendly reminder that the stock price reaction after earnings might have nothing to with how well/bad the company performed during the quarter.

If you have any companies that are reporting earnings next week and want them to be included, let me know in the comments. And if you’d like, you can subscribe to my Youtube channel below (approaching 20K!).

I’ll stop wasting your time now and get right into the companies.

Tuesday, 18 October

Netflix

Revenue grew 16% YOY to $7.5 billion

EPS $3.19 vs est $2.56

Operating Income rose 33% to $1.8 billion.

Netflix added 4.4m paid net adds (vs. 2.2m in Q3’20 and beating their own guidance of 3.5m) to end the quarter with 214m paid memberships.

For Q4’21, we forecast paid net adds of 8.5m, consistent with Q4’20 paid net additions. For the full year 2021, we forecast an operating margin of 20% or slightly better.

This means that Q4’21 operating margin will be approximately 6.5% compared with 14% in Q4’20.

Net cash generated by operating activities in Q3 was $82 million vs. $1.3 billion in the prior-year period FCF for the quarter was -$106 million vs. $1.1 billion in Q3‘20.

FCF in last year’s Q3 was helped by COVID-related production shutdowns. YTD FCF is $410m.

Nothing new regarding games.

Squid Game is their best ever show (more on that in the video)

Growth story is FAR from over.

Netflix Earnings Report

Stock ended the week up 5.17%

Wednesday, 19 October

ASML

Full report here

Q3 net sales of €5.2 billion up 30% YOY misses by €30 million

Gross margin of 51.7%, net income of €1.7 billion

Q3 net bookings of €6.2 billion

ASML expects Q4 2021 net sales between €4.9 billion and €5.2 billion and a gross margin between 51% and 52%

EPS of €4.27

Notes from the call I thought were important.

EUV revenue growth of around 35% year-on-year, an increase from the 30% expected last quarter.

Total backlog to €17.5 billion (EUV €10.9 billion).

ASP was stronger than the previous quarter.

Stock ended the week up 3.4%

Tesla

Full report here and Tesla Daily video

Automotive sales came in at $12.05 billion growing 58% YOY (yeah I guess Tesla isn’t growing anymore…).

Energy sales came in at $806 million growing 39% YOY

Services & others came in at $894 million, growing 54% YOY.

Total sales = $13.57 billion, growing 57% YOY.

Automotive GM = 30.8% (excl. credits)

EPS of $1.86 up 145% YOY

FCF of $1.32 billion

Production & Deliveries

Stock ended the week up 6.8% (officially a +20 bagger for me!)

Thursday, 20 October

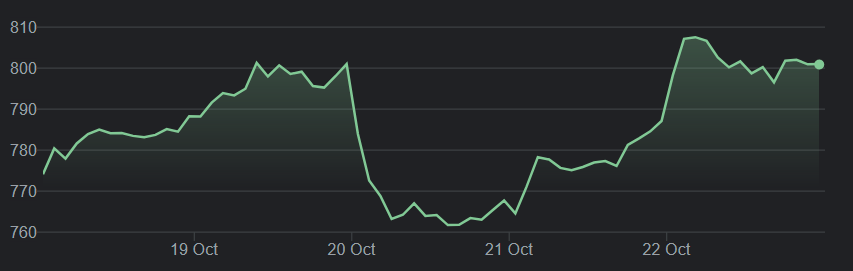

Snap Inc.

Full report here

“The red fruit from the tree is the one who did most of the damage”- Aristotle

Reasons for the miss.

Apple

Supply chain

Apple

Q3 EPS $0.17 vs est. $0.08

Revenue increased 57% YOY to $1.067B v est. $1.1B

DAUs were 306 million in Q3 2021, an increase of 57 million, or 23%, YoY

Year-over-year growth in DAUs has exceeded 20% for four consecutive quarters

Adjusted EBITDA improved 209% to $174 million.

Outlook for Q4 2021 - revenue to be between $1.17-1.21B vs est. $1.36B

Stock ended the week down 29.85% (oops)

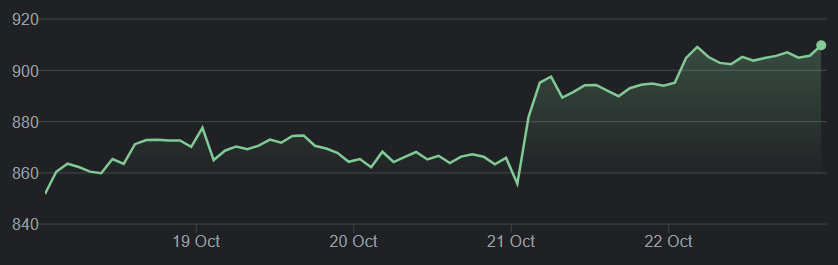

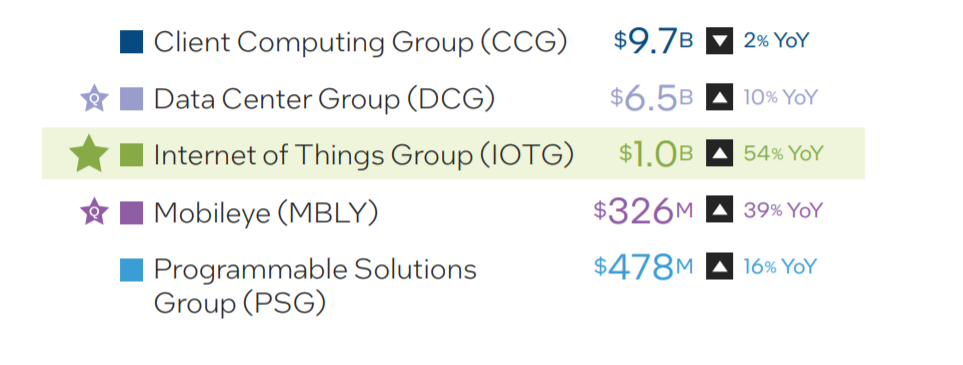

Intel

I go over most of it in the video + some indications of how they plan on taking on AMD and Nvidia.

The company reported EPS of $1.71, an increase of 59% year over year, which beat its own guidance by $0.61.

Revenue came short at $18.1 billion, growing 5% YOY but missing estimates by $0.1 billion.

Gross margin was 57.8%, 2.8 percentage points above guidance, and up 1.3 percentage points YOY.

In the third quarter, the company generated $9.9 billion in cash from operations and paid dividends of $1.4 billion.

The Client Computing Group (CCG) was down due to lower notebook volumes due to industry-wide component shortages, and on lower adjacent revenue, partially offset by higher average selling prices (ASPs) and strength in desktop (and probably AMD taking some market share).

But the big reason the stock fell close to 10% (besides the small miss on revenue) is that the company expects gross margins to be lower for the next two or three years as it continues to invest heavily (something they already announced last Q).

Full-year revenue outlook remains unchanged at $73.5 billion, and Intel expects EPS to be $5.28, up 4% YOY and an increase of $0.48 from prior guidance.

Stock ended the week down 8.7%

If you liked it please do share it! See you all next week!