Earnings Week (7/26 - 7/30)

A week full of surprises

Hey reader!

This is the second edition of the earnings recap series(so bear with me). If you missed last week's recap you can read it here. And if you’d like, you can subscribe to my Youtube channel below.

This week has seen all of the big tech companies report earnings, and as you might have guessed, most beat estimates (by a lot). But that didn’t stop the market from turning red.

I’ll stop wasting your time now and get right into the companies.

Monday, July 26

TESLA 🚗

Full Q2 report here

Delivered units: 201,304

Revenue: $11.96B vs Est $11.36B up 98% YoY

Automotive sales of $10.2B up 97% YoY

Energy sales of $801M up 116% YoY

Bitcoin-related impairment of $23M

Automotive GM% : 28.4% (25.8% Ex Credits) up 3.0% YoY

Energy GM% : 2.5% 20m in profit

Total gross profit of $2.88B up 128% YoY

Net income GAAP of $1.14B up 920% GAAP EPS YoY

EPS $1.45 vs. Exp $0.97 up 233% YoY

Q2 FCF of $619M vs est -319M up 48% YoY

Tesla ended the quarter with $16.2b in cash and cash equivalents.

Outlook

No prediction of when 4680 will be ready for volume. The backup plan is non-structural and 2170.

Demand is not a problem, supply is. FSD progress is being made but the wide release will take time. No real insights on the subscriptions yet.

Tesla will open supercharger network to other manufacturers. Megapack sold out to end of next year. Chance of hitting 1 million powerwalls next year, 20k/week.

Texas and Berlin production will start in 2021. Semi-truck delayed until 2022.

Tesla ended the week up 5.59%

Tuesday, July 27

Starbucks ☕

Full report here

EPS: $1.01 vs. $0.77 est.

REVENUE: $7.5B vs. $7.23B est.

+5000 stores in China, global store count 33.295

24.2m active Starbucks reward membership in the US up 48% (Starbucks is more of a bank than a coffee shop)

Starbucks ended the week down 3.4%

Microsoft:

Full report here

Revenue: $46.2B beating expectations of $44.1B

EPS: $2.17 beating expectations of $1.9

Net income was $16.5 billion and increased 47%

Our commercial cloud revenue grew 36% year over year to $19.5 billion.”

Azure rev Q4FY21: $33B, +51%

Microsoft ended the week down 1.38%

Google:

Full report here

EPS: Q2 EPS $27.26 vs. $19.34 Est

Q2 Revs. $61.88B vs. $56.16B Est

Operating margin: 31%

Operating income: $19.3bln vs $6.3bln in 2020

Google ended the week up 1%

Teladoc:

Full report here

@StockMarketNerd summarized the print very well, you can find it here

Teladoc ended the week down 1.6%

Apple 🍎

Full report here

EPS $1.30 Beats $1.00 Estimate

Sales $81.40B Beat $72.93B Estimate up 36% YoY.

- 63.9bln product

- 17.4bln services

Q3 Sales To Americas Region $35.87B, Up From $27B YoY

Q3 European Sales $18.943B, Up From $14.173B YoY

Q3 Services Revenue $17.486B, Up From $13.156B YoY

Q3 Greater China Sales $14.762B, Up From $9.329B YoY

Q3 Japan Sales $6.364B, Up From $4.966B YoY

IPhone: $39.57B up 49.8% YoY

Mac: $8.24B up 16.38% YoY

IPad: $7.37B up 12% YoY

Wearables, Home, and Accessories: $8.78B up 36.12% YoY

Apple ended the week down 1.6%

AMD 💽

Full report here

EPS $0.63 Beats $0.54 Estimate

Sales $3.85B Beat $3.62B Estimate

Gross margin 48%

Op income $831M; Non-GAAP $924M

Op margin 22%; Non-GAAP 24%

Net income $710M; Non-GAAP $778M

Operating cash flow $952M;

Record FCF $888M

Repurchased 3.2M shares of common stock for $256M

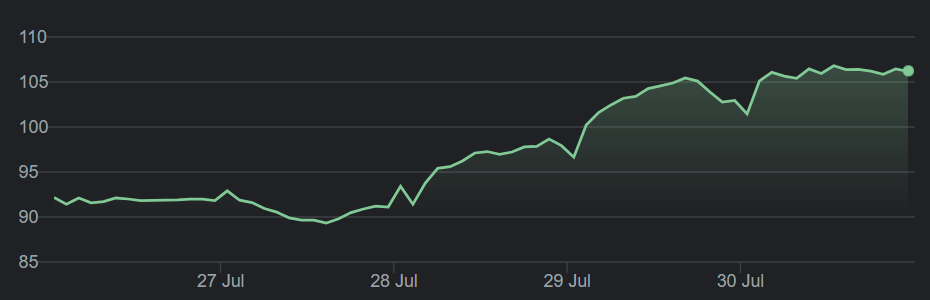

AMD ended the week up 15.2%!

Wednesday, July 28

Shopify 🛒

Full report here

filed a $10B shelf offering.

Rev $1.12bln up 57% YoY

- Subs solutions $334M up 70% YoY

- Merchant solutions $785M up 52% YoY

GMV for Q2: $42.2bln up 40% YoY

GPV $20.3bln up 45% YoY

Adj operating income: $236.8M up 16% YoY

Adj net income: $284.6M or $2.24 eps

$7.76 billion in cash, cash equiv.

Shopify ended the week down 9%

Spotify 🎶

Full report here

165M paid subs (top end of forecast)

365M MAUs (below guidance)

Podcast revenue was up over 627%

")

Outlook:

Q3:

Total MAUs: 377-382 million

Total Premium Subscribers: 170-174 million

Total Revenue: €2.31-€2.51 billion

Q4:

Total MAUs: 400-407 million

Total Premium Subscribers: 177-181 million

Total Revenue: €2.48-€2.68 billion

Spotify ended the week down 3.9%

Facebook:

Full report here

The metaverse was the center of attention during the call. It was also in Mark’s first remarks.

It’s safe to say that Facebook is very focused on investing in the metaverse or what the metaverse could be.

Revenue: $28.58B Beat $27.82B Estimate up 56% YoY

EPS: $3.61 Beats $3.02 Estimate up 101% YoY

Daily active users (DAUs) 1.91B vs est. 1.91B an increase of 7% YoY

Monthly active users (MAUs) 2.90B vs est. 2.90B an increase of 7% YoY

Family monthly active people (MAP) was 3.51 billion as of June 30, 2021, an increase of 12% YoY.

Operating margin up to 43% YoY from 32%

Net income up 101% YoY to over $10B (net income was up 100% YoY in Q2 of 2020 as well)

Outlook:

In the third and fourth quarters of 2021, we expect year-over-year total revenue growth rates to decelerate significantly on a sequential basis as we lap periods of increasingly strong growth. When viewing growth on a two-year basis to exclude the impacts from lapping the COVID-19 recovery, we expect year-over-two-year total revenue growth to decelerate modestly in the second half of 2021 compared to the second quarter growth rate.

We continue to expect increased ad targeting headwinds in 2021 from regulatory and platform changes, notably the recent iOS updates, which we expect to have a greater impact in the third quarter compared to the second quarter. This is factored into our outlook.

Facebook ended the week down 3.5%

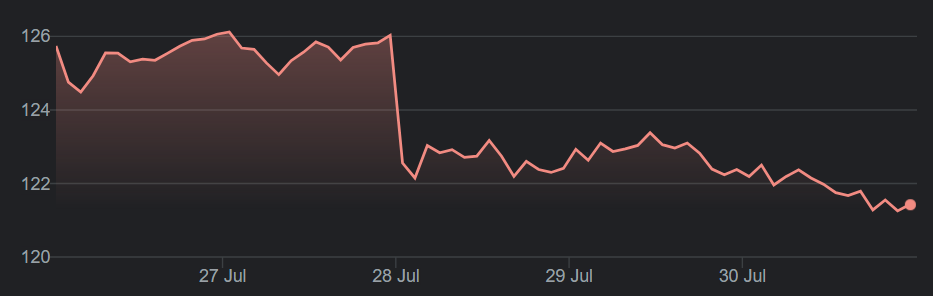

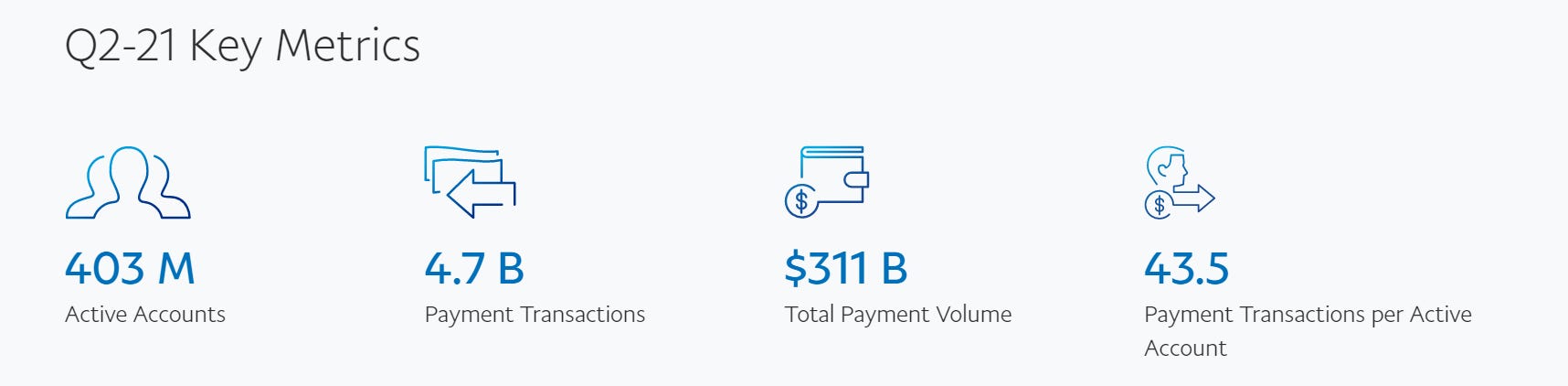

Paypal 💳

Full report here

Q2 EPS $1.15, vs est. $1.13

Revenue $6.24B vs est. $6.27B

Venmo processed approximately $58 billion in TPV, growing 58%

Merchant Services volume grew 48% on a spot basis, and 43% FXN, representing 96% of TPV

eBay Marketplaces volume declined (37%) on a spot basis, and (41%) FXN, representing 4% of TPV, compared to 9% in the prior-year period

43.5 payment transactions per active account on a trailing twelve months basis, growing 11%

Outlook:

Q3 2021 EPS $1.07 vs est. $1.14

Q3 2021 revenue $6.15-6.25B vs est. $6.43B

FY2021 EPS $4.70 vs est. $4.73

FY2021 revenue $25.75B vs est. $25.88B

Paypal ended the week down 11%

Thursday, July 29

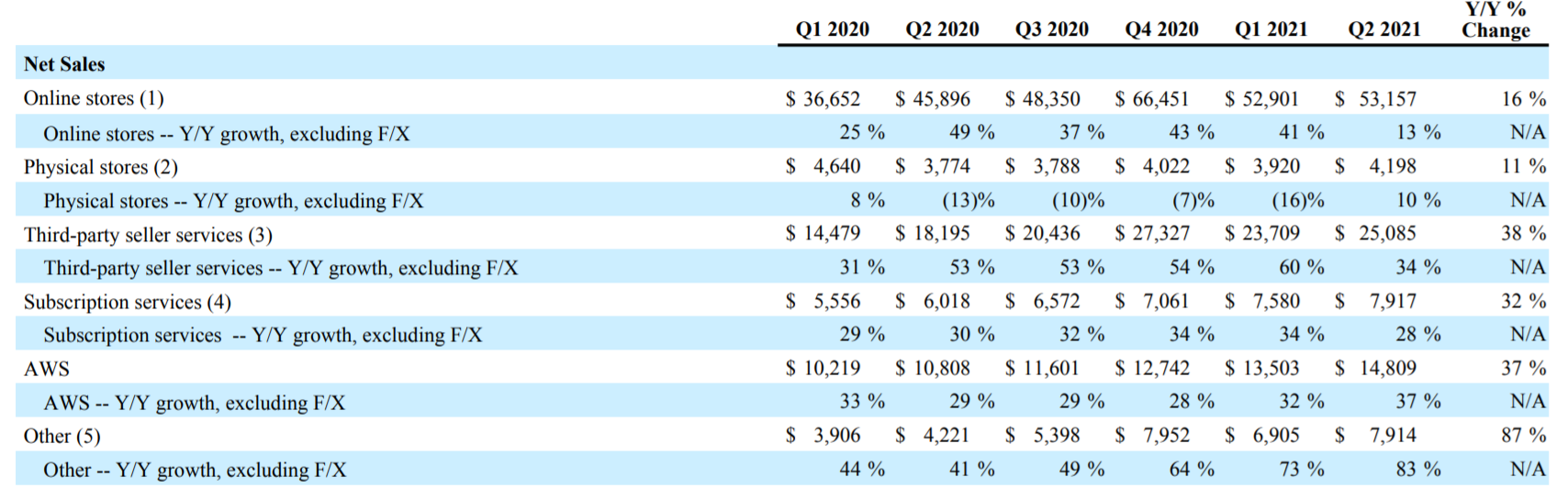

Amazon:

Full report here

Net sales $113.1B (+27% YoY) vs. $115.20B Est

Q2 EPS $15.12 vs. $12.30 Est.

Net income $7.8B, +50%

Low margin e-commerce sales growth slowing, but high-margin segments all crushing it:

AWS $14.8B, +37%

Advertising $7.9B, +83%

Subs $7.9B, +28%

Faster growing segments are now $56bln in Sales vs. slower at 57 bn.

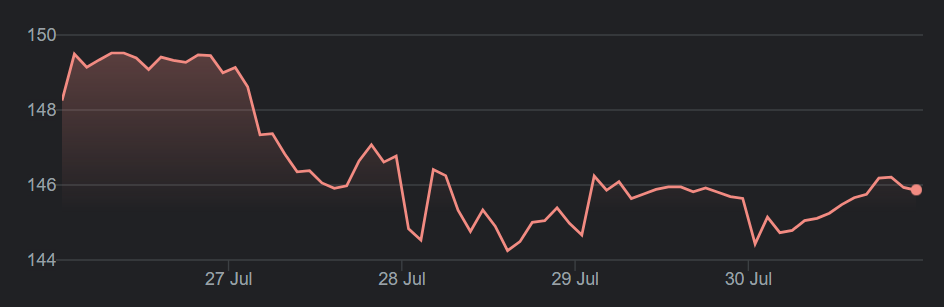

Amazon ended the week down 9.4%

Pinterest: 📌

Full report here and Youtube video here

Revenue up 125% YoY to $613 million and 26% QoQ

Q2 EPS $0.25, vs est. $0.13

Global MAU up 9% down 5% QoQ

US MAU down 5% YoY and 7% QoQ

International MAU up 13% but down 4.5% QoQARPU global up 89% 27% QoQ

ARPU US 103% YoY 27.32% QoQ

ARPU International up 163% YoY and 38% QoQ

Net income: $69.4M

Adjusted EBITDA: $178.2

Increase in revenue. More advertisers. Investment in shopping is working. In Q2, MAUs on our mobile apps grew in the U.S. year over year and grew by more than 20% internationally. Web users (least engaged audience) are responsible for the decline. Gen Z's audience grew double-digits YoY. Shopping engagement is more resilient than overall engagement

No guidance for Q3 MAUs, expecting revenue in the low 40% growth YoY

Pinners that save items to their shopping list are 7x more likely to buy things. Finally, the plan to pilot seamless on-platform transactions by the end of the year is on track.

Pinterest ended the week down 22.6%

That’s it for this week! If you liked it please do share it!